Credit Acceptance

More than just a lender: how a misjudged asset has forged one of the most resilient compound capitalization machines on the market.

Thesis Summary

In a market that excludes more than 140 million Americans, Credit Acceptance has built a competitive moat over 50 years, generating exceptional returns by serving the underserved. Despite regulatory risks, negative market perception creates an opportunity to invest in a high-quality, resilient compounding machine at an attractive price.

Introduction: A fortress hidden behind a bad reputation

My interest in Credit Acceptance began in 2020, while reading the annual letters from Rob Vinall, one of the investors I most admire. In his 2014 letter, he revealed his latest investment: a company with a name that at first glance generates skepticism, operating in the reviled niche of subprime auto loans. A quick look at the stock’s impressive performance since then confirmed my suspicion: behind the controversial facade, there must be an exceptional business.

What I discovered upon investigation was that, behind its bad reputation, the company was addressing a fundamental reality in the United States: for a large part of the population, a car is not a luxury, but an indispensable tool for progress. It is a means of getting to work and achieving economic stability.

The traditional financial system, however, denies this tool to 56% of the adult population, creating a huge structural gap. It is in this void that Credit Acceptance operates, offering not only a loan, but a second chance to build a credit history and, ultimately, improve one’s long-term financial situation. This thesis delves into this paradox to reveal how, behind the market’s prejudices, lies a financial strength of the highest quality.

The story: The birth of a real problem

Credit Acceptance was founded in 1972 by Donald Foss in Southfield, Michigan. At the time, Foss owned and operated one of the largest used-car businesses in the United States. Foss identified a structural problem in the market: many customers with low or no credit history were unable to obtain financing to purchase a vehicle. This resulted in lost sales for dealerships, which turned away customers due to lack of financing.

Foss’ solution was ingenious: instead of lending money like a traditional bank, he created a partnership model with the dealerships. Credit Acceptance financed the subprime buyer and shared the risk with the dealership. This allowed dealerships to sell vehicles they previously could not, while Credit Acceptance recovered its returns gradually over time through the borrower’s payments. This system turned Credit Acceptance into a bridge between high-risk consumers and dealerships, laying the foundation for a unique model in the industry.

During the 1980s, Credit Acceptance consolidated its network of affiliated dealerships in the United States and refined its credit risk management model, focusing on collection discipline and borrower analysis.

In 1992, the company took a key step by going public on the NASDAQ under the ticker symbol CACC. This move allowed the company to raise additional capital to acquire more contracts, validate its model with institutional investors, and strengthen its financial structure.

During the 1990s, Credit Acceptance rapidly expanded its network of affiliated dealerships, which became its main channel for growth. Later, in the 2000s, the subprime auto market began to gain relevance. Credit Acceptance specialized in this niche, differentiating itself from companies such as Ally Financial (more focused on prime) or traditional banks.

It based its model on three fundamental pillars:

This model allowed Credit Acceptance to remain profitable.

In 2008, the financial crisis hit, which was a litmus test for the company. While banks and traditional financial institutions restricted credit, Credit Acceptance continued to operate in the subprime market.

As a small player compared to systemic banks, it did not depend on structured products or the mortgage market.

Many customers who had lost access to traditional credit turned to this type of lender.

The result: the company not only survived but demonstrated resilience and reinforced its reputation as a subprime specialist.

After the 2008 financial crisis, the company entered a golden decade. The subprime market grew because millions of consumers had been left out of the banking system. Credit Acceptance expanded its portfolio and dealer network. Its revenues and profits multiplied.

What most attracted investor’s attention was its capital policy. It allocated its profits to share buybacks and between 2010 and 2020 withdrew a very high percentage of its outstanding shares.

This boosted the company’s earnings per share and became a case study among fund managers.

More recently, we have seen growth accompanied by greater scrutiny.

In 2020, the Federal Trade Commission (FTC) and the state of Massachusetts sued the company, accusing it of hiding the real costs of loans and inflating the prices of financed cars. Since then, regulatory pressure has intensified and is one of the key risks for the future.

Despite this, it remains one of the undisputed leaders in the subprime automotive segment in the United States and has strengthened its risk analysis systems with big data and predictive models, adapting to new technologies.

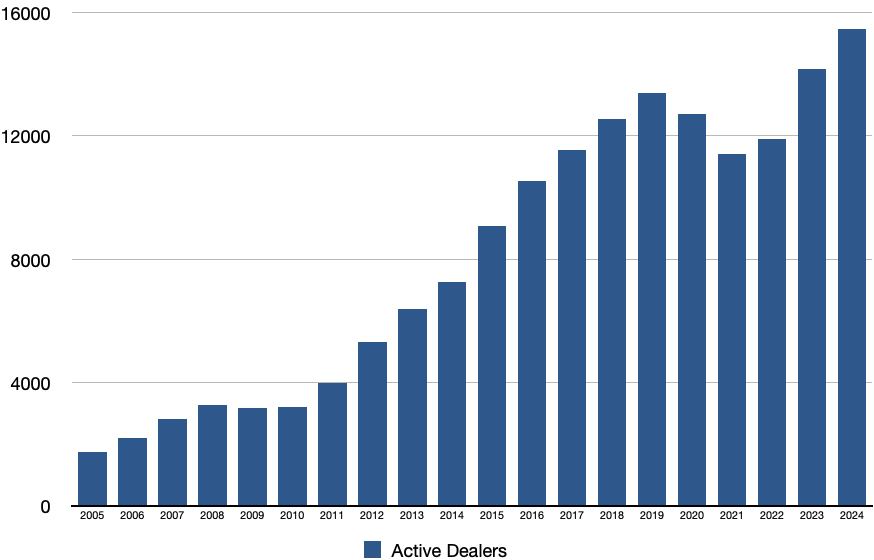

Today, Credit Acceptance reaches its 50th anniversary as a proven model, but in an increasingly regulated sector under the scrutiny of legislators and consumers. Credit Acceptance has continued to increase its affiliated dealerships and expand its portfolio of financed contracts, currently boasting 15,463 active dealerships.

The engine of the business: dealer financial programs

The network of affiliated dealerships is at the heart of Credit Acceptance’s business model. The company does not sell directly to end consumers but enters into partnership agreements with car dealerships (both independent and franchised) throughout the United States.

The operation is based on two main programs:

Portfolio Program

Credit Acceptance shares the loan payments with the dealership.

The dealer receives a reduced down payment at the time of sale but retains a share of future cash flows. This gives the dealer a direct incentive to place higher-quality loans and collaborate in risk management.

Purchase Program

Credit Acceptance purchases the financing contracts directly from the dealer, paying a larger sim immediately. In this case, the company assumes al credit and collection risk, while the dealer obtains quick liquidity.

Both programs seek to align the interest of the company and the dealers.

The Portfolio Program encourages long-term cooperation and responsible customer selection.

The Purchase Program offers flexibility to dealers who prefer immediate cash to rotate inventory.

Thanks to this structure, Credit Acceptance has become a key partner for dealers seeking to expand their customer base, allowing them to sell vehicles to people who would not have access to traditional credit.

Why is it in the dealers’ interest to affiliate with Credit Acceptance?

Dealers partner with Credit Acceptance because the company offers them immediate access to subprime customers while ensuring liquidity and inventory turnover, something they would struggle to achieve on their own.

Key benefits for dealerships:

Sell more cars

An affiliated dealership can close sales with customers who would otherwise be rejected by banks or traditional financial institutions. This allows them to expand their potential customer base and increase the number of units sold per year.

Immediate liquidity

Thanks to advance payment, the dealer receives money when the car is sold and does not have to wait 3-4 years for the customer to pay off the entire loan. This allows them to rotate inventory quickly and purchase more cars to continue selling.

Reduced risk of non-payment

In the Purchase Program, the dealer transfers 100% of the risk to Credit Acceptance. In the Portfolio Program, although the dealer participates in the contract, most of the risk is absorbed by Credit Acceptance.

Additional income in the Portfolio Program

In addition to the down payment, the dealer participates in the customer’s future payments. If the customer complies, the dealer can earn more money than in a traditional sale.

Administrative simplicity

Credit Acceptance handles collections, account management, recoveries in case of non-payments, and legal matters. The dealer is relieved of this burden and can focus on selling cars.

Reputational effect and credibility

Being associated with a national, publicly traded financial institution reinforces customer confidence and improves the dealership’s image.

In conclusion, dealerships partner with Credit Acceptance because it allows them to sell more, get paid sooner and take on less risk.

The opportunity cost of not joining is high: losing customers who can finance their car with another affiliated dealership.

Structure of financing contracts

The structure of Credit Acceptance’s financing contracts is characterized by its flexibility and the way it distributes risk between the company and the dealerships. The main objective is to allow customers with low or no credit to access a vehicle, while the company maintains a profitable model in a high-risk segment.

The company works with two main contractual arrangements: Portfolio Program and Purchase Program.

Portfolio Program (contract participation)

This is the program most used by the company, currently accounting for 78.7% of total revenue.

The dealer receives a smaller down payment but retains a percentage of future loan payments.

The dealer and Credit Acceptance share the risk: if the customer pays on time, the dealer earns more revenue over time.

This aligns incentives, as it motivates the dealer to select customers with higher credit quality and maintain good sales practices.

Purchase Program (direct purchase of the contract)

This program accounts for 21.3% of total revenue and is becoming decreasingly used because it misaligns the dealer with Credit Acceptance throughout the loan, which can result in poor quality loans as the dealer needs to sell.

The dealer sells the vehicle and Credit Acceptance immediately purchases the financing contract.

The dealership receives a higher upfront payment, obtaining liquidity to rotate its inventory quickly.

Credit Acceptance assumes all credit risk: it is responsible for collections, delinquency management, and recovery in the event of non-payment.

This model is attractive to dealers who prioritize immediate liquidity over future income.

Both programs include conditions typical of subprime loans:

High interest rates to offset the risk of default.

Variable repayment terms, although generally shorter than those of prime loans.

Possibility of incorporating insurance, extended warranties and additional charges that increase the total cost of the loan.

The key to Credit Acceptance’s use of this model is that it diversifies risk across thousands of contracts and dealerships, structures cash flows so that initial collections cover a large portion of the risk and leverages its know-how in recovery and collection to maximize the recovery of delinquent loans.

Collection and payment recovery process

Credit Acceptance’s business model relies heavily on its collection system. Unlike traditional institutions, the company does not only grant loans but has developed a robust infrastructure over more than 50 years to manage defaults and maximize recovery in a high-risk segment such as subprime.

This process consists of three levels:

Preventive collection and early management

From the outset, customers receive frequent payment reminders (SMS, reminder calls).

The company uses predictive risk models based on big data to identify customer profiles that are likely to fall behind and take action before default occurs.

The goal is to keep the customer up to date with payments and prevent the loan from becoming delinquent.

Active collection in case of delays

If a payment is missed, Credit Acceptance has a legal and operational team specializing in debt recovery. The contract usually allows for additional late fees to be applied, which increases profitability if the consumer ends up settling the situation. At this point, if the Portfolio Program has been used, the dealer has a financial incentive to collaborate in the recovery, as their income depends on the flow of payments.

Recovery through courts and seizures

One advantage that sets Credit Acceptance apart is its extensive use of legal proceedings to recover debts.

The company often files civil lawsuits against delinquent customers, obtaining court judgements that allow it to garnish wages, bank accounts, or other assets.

Although this process is costly, the scale and experienced accumulated allow it to do so profitably, recovering significant percentages even in cases of prolonged delinquency.

Revenue model

Credit Acceptance’s model is based on transforming high-risk loans into predictable and profitable cash flows, combining interest, fees and judicial recoveries. Unlike traditional banks, its success does not depend solely on the customer’s initial ability to pay, but on the effectiveness of comprehensive loan cycle management.

First, interest on loans.

This accounts for most of the company’s revenue, as the loans granted by Credit Acceptance tend to have high interest rates to compensate for the higher risk of default.

These fees generate high gross margins, even if some of the customers default.

Secondly, additional fees and charges.

This section includes insurance, extended warranties, and late payment fees. This secondary income increases profitability per contract, as in some cases it accounts for a significant portion of the recovery.

Third, the share of contracts under the Portfolio Program.

In this program, the dealer shares the future cash flows of the loan with Credit Acceptance.

For the company, this represents a variable but attractive source of income, which is supported by the quality of the selected customer and aligned with the dealer’s incentives.

Finally, the management of legal recoveries.

When a loan goes into definitive default, the company does not write off the debt as a loss but activates legal mechanisms for its recovery. Favorable rulings allow for the seizure of wages, bank accounts, or asset recovery, generating additional long-term cash flows.

Thanks to its accumulated experience and know-how, Credit Acceptance can model risk with pinpoint accuracy. The data validates the robustness of the model: over the last 20 years, the variance between the initial collection forecast and actual collection has been just 0.3%.

Credit market

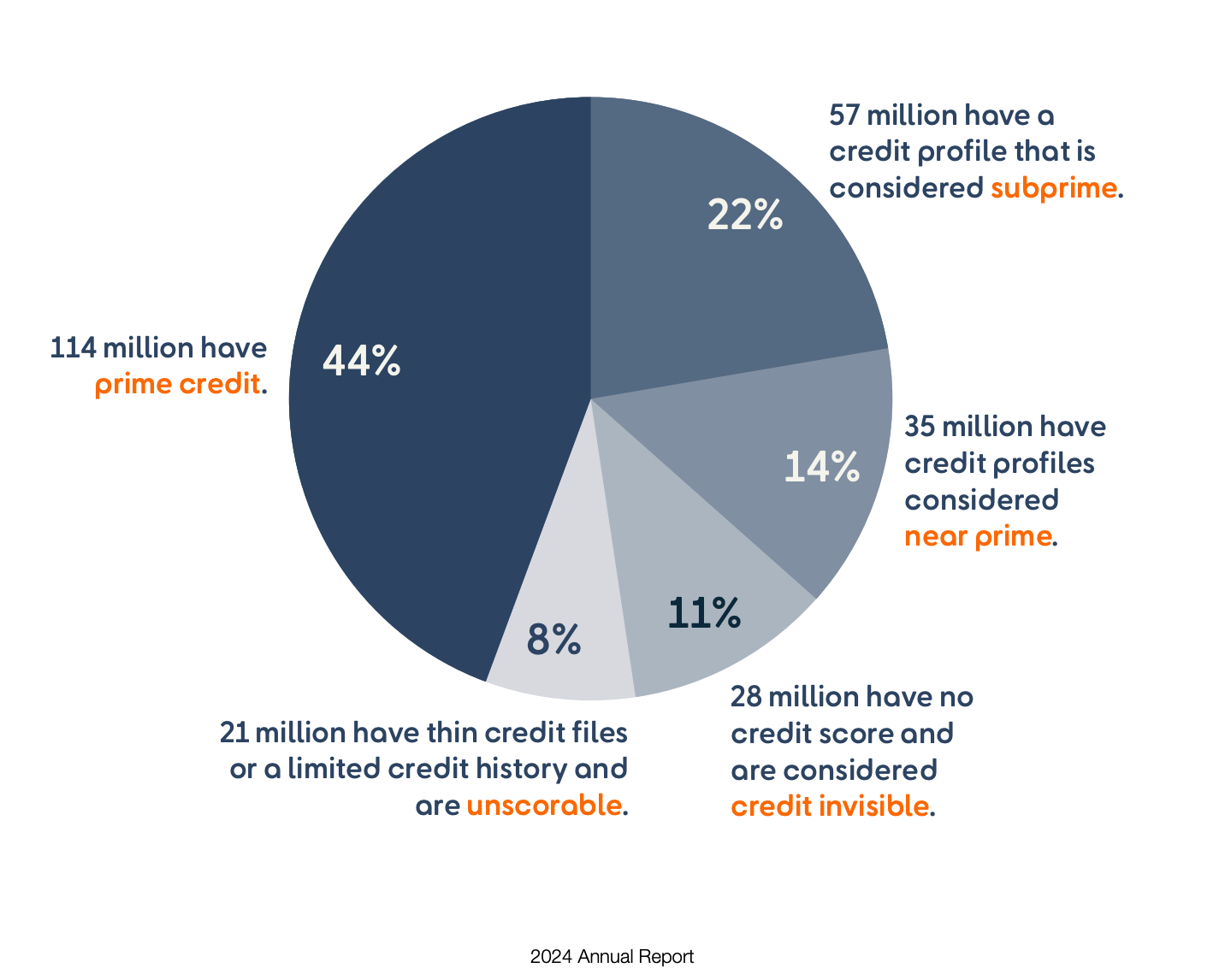

The U.S. financial system, which encompasses 257 million adult consumers, is structured around the preeminence of the FICO score as primary risk assessment tool. While this model standardizes credit granting, its rigidity creates structural exclusion for a significant portion of the population, resulting in a deep gap in access to financing.

An analysis of the distribution of credit profiles clearly reveals this gap.

Only 44% of consumers, or 114 million people, have a prime credit rating, which guarantees them full access to traditional banking products and services.

The remaining 56%, more than 140 million people, face varying degrees of financial exclusion, forming a vast underserved market. This group breaks down as follows:

22% are considered subprime (57 million).

14% are classified as near-prime (35 million).

11% lack sufficient credit history to be evaluated (28 million).

8% have credit records that are too limited to generate a score (21 million).

This phenomenon creates a structural credit gap in the U.S. market, where millions of consumers with the ability and need for financing are systematically excluded from the conventional banking system.

It is precisely in this niche market, neglected by traditional banks, that non-bank financial institutions such as Credit Acceptance operate. The company has designed its business model to offer auto financing solutions to subprime and unrated segments.

Credit Acceptance’s strategic positioning is clear: rather than competing directly with banks for the prime segment, it positions itself as an essential player for consumers with greater barriers to credit access. The company takes a calculated and significantly higher risk, which is offset by higher returns, thus becoming a key part of the financing ecosystem for a disadvantaged segment of the population.

Case study of a Credit Acceptance loan

Henry Lopez, a resident of Detroit, needs a car to get to his new job. He finds a used vehicle at a local dealership for $10,000.

Henry has an irregular credit history: in the past, he defaulted on a personal loan, and his FICO score is currently below 600. As a result, traditional banks will not grant him financing.

The care is for sale at Johnson Auto Sales; an independent dealership affiliated with Credit Acceptance. The owner, David Johnson, wants to close the sale, but he knows that Henry will not be able to get a loan in the traditional market. Thanks to David’s partnership with Credit Acceptance, he can offer Henry two options.

Portfolio Program:

David receives an initial advance of $7,000 from Credit Acceptance. Henry signs a $15,000 loan to be repaid over 48 months ($10,000 principal plus interest and fees). As Henry makes his payments, David will receive 25% of the collected cash flows.

Purchase Program:

David receives a higher upfront payment, $9,000, at the time of closing the deal. In return, he fully assigns the contract to Credit Acceptance and no longer receives any additional payments. In this case, all future risk and reward remain with Credit Acceptance.

Result: What happens in each scenario?

If Henry makes the payments on time:

In the Portfolio Program, David ends up receiving $10,750 in total ($7,000 + $3,750).

In the Purchase Program, David receives $9,000 immediately, with no additional risk.

Credit Acceptance, for its part, earns a net $4,250 on the Portfolio and $6,000 on the Purchase.

If Henry defaults and only 40% of the loan ($6,000) is recovered:

In the Portfolio Program, David receives a total of $8,500 ($7.000 upfront + $1,500 in participation). The car was worth $10,000, so the dealer will not cover the profit he expected, but he will rotate inventory and secure his margin.

In the Purchase Program, David receives $9,000 regardless of non-payment. Although he gives up $1,000 of the sale price, he can sell that vehicle, increase his inventory, and secure his margin, as these cares are often auctioned for $6,000-$7,000, generating a profit of $2,000-$3,000.

Credit Acceptance, meanwhile, loses $2,500 in the Portfolio and $3,000 in the Purchase model.

Historical profitability

Sales growth

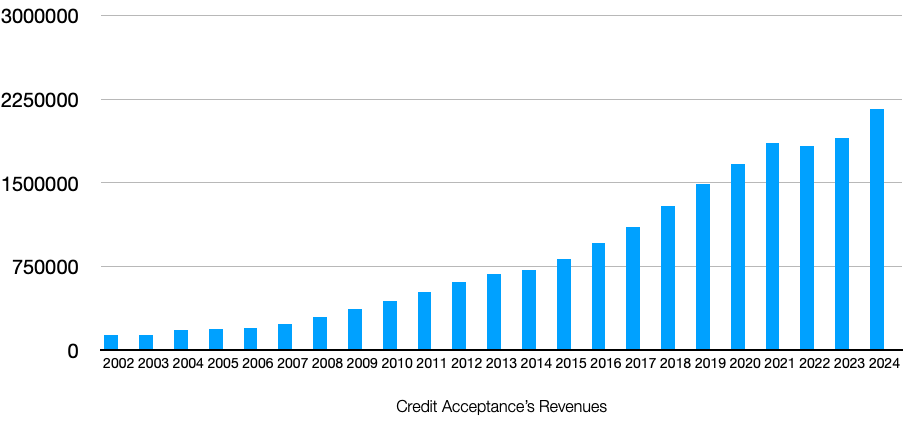

Credit Acceptance’s revenues have grown at an annual rate of 13% since 2002. This is very significant growth for a financial company.

Even during the 2008 financial crisis and the COVID crisis in 2020, the company increased its revenue. Only in 2022 did the company see a 1% decline in revenue.

Growth in earnings per share

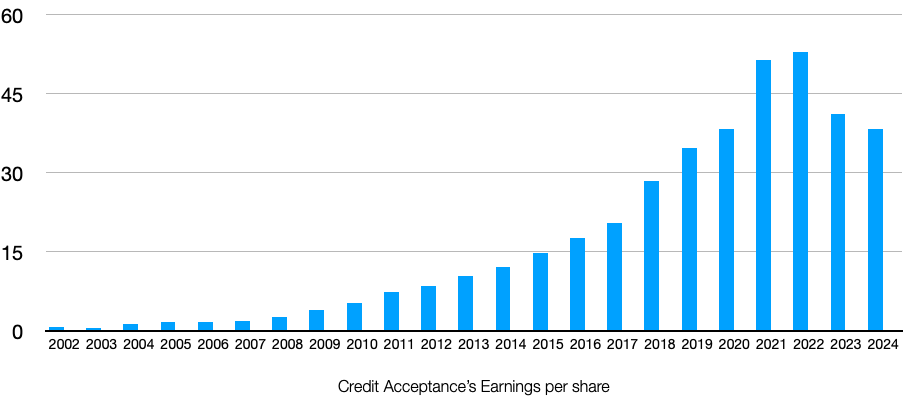

Earnings per share have grown at an annual rate of 19% since 2002. The key to this growth has been the aggressive share buyback program carried out by the management teams over the years.

The resilience of the model is remarkable: the company not only remained stable during the 2008 financial crisis but continued to grow, a trend that was also observed during the COVID crisis in 2020. In recent years, earnings per share have declined because loans originated in 2022 turned out to be worse than expected. This has led to less cash and an increase in delinquencies, which has caused a decrease in earnings per share.

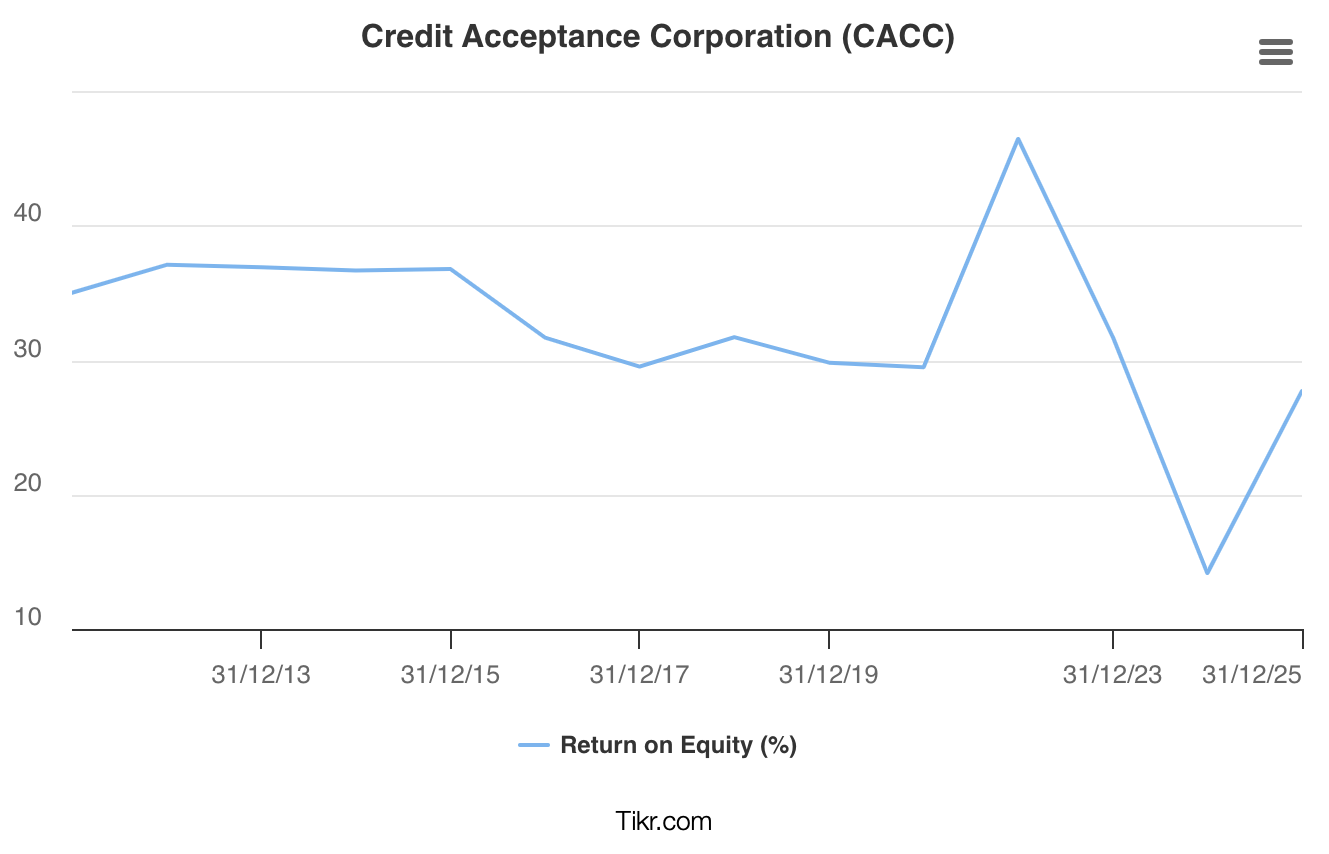

Return on equity

The company has had an average return on equity of 30%. This return is well above the industry average and demonstrates the company’s competitive advantage.

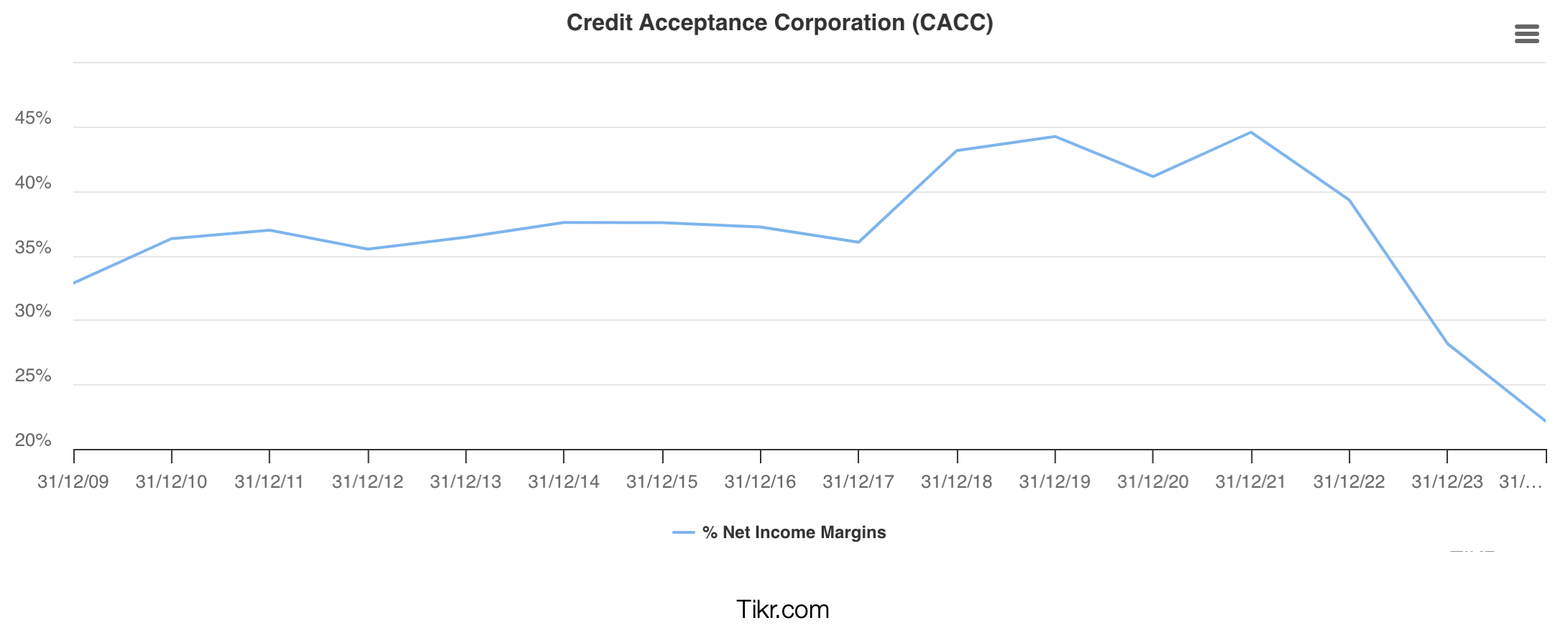

Net profit margins

Net profit margins have been around 35%. From 2018 onwards, the company increased its profit margin above the average, as loans during that period performed better than expected.

However, the 2022 credits were significantly worse than expected, negatively impacting the company’s results, which the management expects to gradually improve over time.

Share buyback policy

The company maintains an excellent share buyback policy, which over time has generated enormous value for shareholders. In its annual letters, the company clearly explains how it decides when to repurchase shares and under what criteria. Its policy is based on the following principles:

Business priority: their first obligation is to finance and reinvest the business itself. Only when there is excess capital is it returned to shareholders, mainly through repurchases and not through dividends.

Valuation discipline: repurchases are only executed when the share price is equal to or below the intrinsic value estimated by the company.

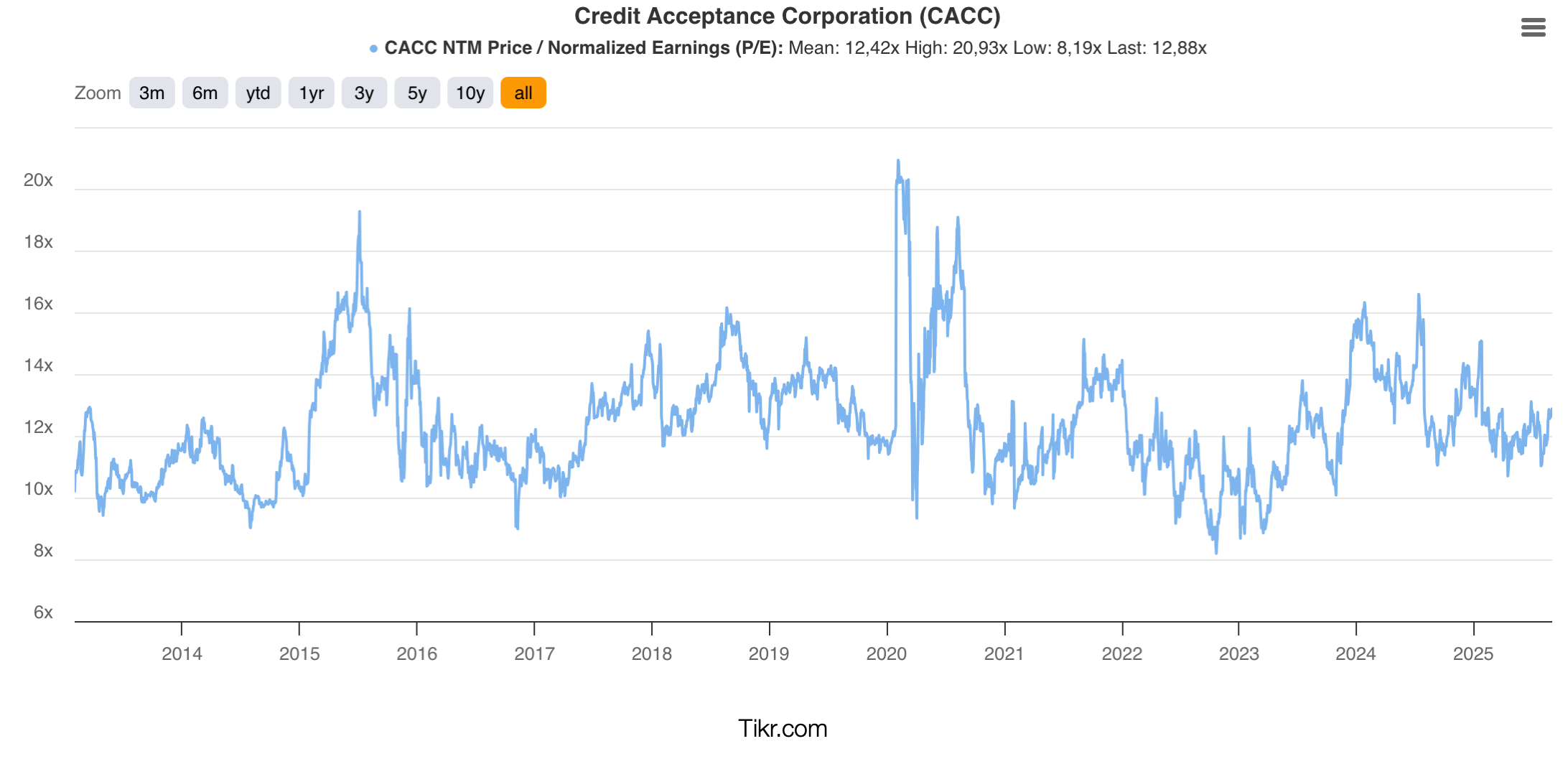

The company has benefited from the fact that the market has historically valued it at an average of 12 times earnings. This multiple has allowed Credit Acceptance to generate immense value, since by acquiring its own shares at relatively low multiples, it significantly increases the value per share for remaining shareholders.

The advantages of this strategy over dividends are clear:

Increase in the value of the remaining shares as the purchase is made below intrinsic value.

Tax advantages: shareholders can defer tax payments if they decide to sell.

Flexibility: shareholders can increase their stake or receive cash, or both, depending on their circumstances.

Transparency in periods without buybacks: the temporary absence of buybacks does not necessarily mean that management considers the stock to be overvalued but may be due to prudent capital assessments or periods of public disclosure.

The case of Credit Acceptance illustrates how a disciplined buyback policy guided by intrinsic value and financial prudence can become a source of sustainable long-term value creation, far superior to a dividend policy.

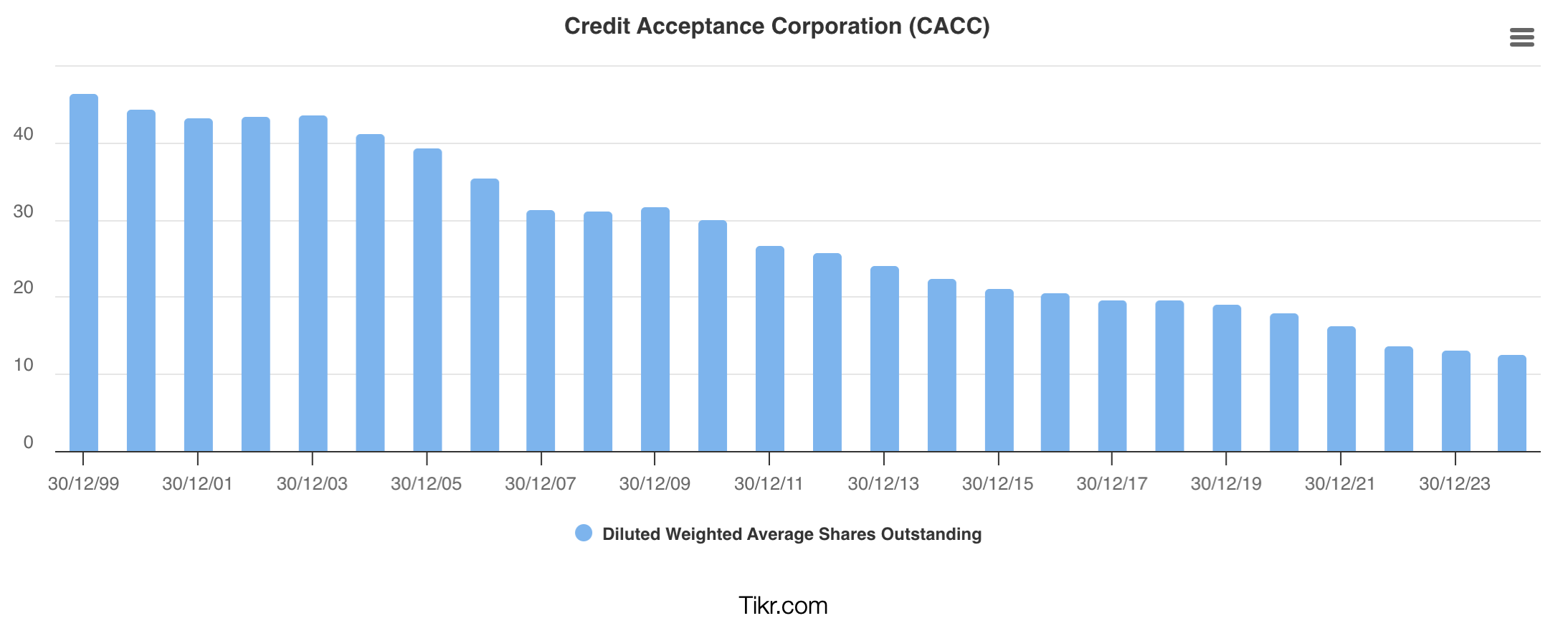

Since 1999, the company has reduced its outstanding shares by more than 85%, by applying an approach typical of large compounders: wait, be patient, and only act when the market offers clear opportunities. More than just an accounting decision, this strategy represents a statement of principles: prioritizing real value creation for shareholders, even when that means going against the market trend.

Debt analysis

Debt structure

Credit acceptance has a diversified debt structure, with secured financing and securitizations (ABS) as its main sources of financing. The most relevant components are:

Secured financing: large-volume loans secured by the company’s own portfolio of loans granted to customers.

Senior notes: long-term bond issues with priority payment and relatively high fixed rates (up to 9.25% in the 2028 issue).

Revolving credit facility: flexible line of credit used marginally and intended mainly for immediate liquidity purposes.

Mortgage note: mortgage loan already settled, with no relevance on the balance sheet.

Overall, the company’s debt is strongly backed by assets (customer loans and restricted cash), which partially reduces the risk perceived by creditors.

Maturity schedule

The maturity profile shows a high concentration between 2025 and 2028:

2025: approximately $500 million.

2026-2027: approximately $2.55 billion in total.

2028: more than $3,300 million, mainly ABS and senior notes

This pattern reflects a significant refinancing risk, as the company must periodically replace large volumes of debt.

Average maturity of assets versus liabilities

Loans granted to customers have an average term of three to five years, in line with the maturities of the main financing instruments.

This alignment between assets and liabilities means that the company does not incur significant maturity mismatches, which is positive from the liquidity and financial stability standpoint.

Types of rates and cost of debt

Most of the debt is fixed rate, reducing exposure to interest rate volatility. Variable-rate debt linked to SOFR is minimal.

However, there has been a gradual increase in the cost of financing: while older issues were placed at rates close to 2-5%, the most recent instruments (such as the 2028 Senior Notes) reach 9.25%. This reflects the impact of the U.S. interest rate environment on the average cost of debt. If interest rates fall, the company will be able to finance itself much more cheaply, so the margin on new loans will increase.

Credit Acceptance has a net debt/equity ratio of 3.4x. This is a high figure, but as it is a subprime financial company, it is quite common in the sector. Levels will need to be monitored; a ratio is considered acceptable if it is below 5-6x. Comparable companies such as Goeasy have a net debt/equity ratio of 3.23x.

The reason for this structurally higher leverage compared to traditional banking is key:

Source of financing: Unlike banks, whose main debt is customer deposits, Credit Acceptance does not take deposits. It finances itself through bonds, credit lines and securitizations (ABS), all of which appear as debt on the balance sheet, inflating the debt/equity ratio.

Profitability model: While banks operate on low margins (2-4%) offset by massive volume, Credit Acceptance achieves very high operating profitability (around 15-20%). To sustain this profitability in a higher-risk business, they use more aggressive leverage.

Capital allocation: banks tend to retain more equity due to regulatory requirements. In contrast, Credit Acceptance returns a large portion of its profits through buybacks or dividends, so equity grows little in proportion to the balance sheet.

Credit Acceptance has a BB rating from S&P and a Ba3 rating from Moody’s. Rating agencies give it this rating because they recognize its strong profit generation and high margins, but they also penalize its high leverage, its dependence on wholesale markets for financing, and its exposure to subprime customers.

In other words, Credit Acceptance is not an “investment grade” issuer, but within the high-yield segment, it is at the top end and relatively stable, reflecting confidence in its model despite structural risks.

Comparable companies

Companies that could be used as comparables for Credit Acceptance include Goeasy in Canada and World Acceptance in the United States.

Goeasy

Goeasy (TSX: GSY) is a Canadian financial company specializing in providing credit solutions to the non-prime segment of the population, i.e., consumers who do not qualify for traditional financing due to their credit history.

Founded in 1990 and headquartered in Mississauga, Ontario, the company has built a diversified business model that encompasses unsecured personal loans, secured home equity loans, point-of-sale financing, and lease-to-own financing.

Goeasy has two business models: easyfinancial and easyhome.

Easyfinancial provides unsecured and secured personal loans to non-prime consumers. Due to the non-prime risk profile, they can charge higher interest rates to offset expected delinquencies and losses. This segment accounts for most of the company’s revenue and loan portfolio.

Easyhome offers consumer products (appliances, furniture, etc.) under a lease-to-own model, also targeting consumers with limited access to traditional credit.

Both divisions are supported by a network of more than 400 physical branches and a growing digital presence. The omnichannel strategy allows it to attract customers more efficiently and offer products tailored to their risk profile.

Goeasy finances its portfolio primarily through corporate debt (unsecured bonds), combined with lines of credit and retained earnings. As it has grown, it has managed to improve its credit ratings and reduce financing costs, which has been key to maintaining its profitability in its high-risk segment.

Goeasy has a total loan portfolio of CAD 4.6 billion and total revenues of CAD 1.52 billion. The annualized net charge-off rate is 8.9%, and the allowance for credit losses stands at 7.61%. The company reports a return on equity of 24.9%.

Goeasy, like Credit Acceptance, operates with high margins to offset risk, allowing it to charge fees, interests and charges that compensate expected losses. It has diversified revenues and operates on a growing scale.

Goeasy’s main risks are like those of Credit Acceptance, as delinquency or losses can be a major threat to the company. In addition, high debt costs reduce the operating margin. At the same time, they have a regulatory risk, just like Credit Acceptance. They depend on physical channels, which increases fixed costs.

World Acceptance

World Acceptance (NASDAQ: WRLD) is a U.S. consumer lending company that focuses on customers with limited access to traditional bank credit. Founded in 1962 and headquartered in Greenville, South Carolina, it operates primarily through a network of more than 1,000 branches in 16 states, with a model focused on personal installment loans.

It offers short- and medium-term personal loans with periodic payments to subprime and underbanked consumers. It operates through physical branches with personal contact and collection follow-up. It has complementary services such as insurance, tax preparation, ancillary products, and so on.

In recent years, it has prioritized a strategy with long-standing customers with better credit histories and has sought to reduce high-risk loans.

World Acceptance has grown its revenue by 6% over the last 23 years and its earnings per share by 12% thanks to its history of share buybacks. It has an average ROE of 15%. It currently has a loan portfolio of $1.85 billion and total revenues of $564 million. Its delinquency rate for loans more than 61 days past due is approximately 5.5%, which it manages to reduce to 3.5% at 90 days, thanks to its strategy of larger loans and its focus on existing customers.

Its business model has strengths and risks like those of Credit Acceptance.

These two companies illustrate that, while operating differently within the same sector, it is possible to obtain distinct yet equally positive outcomes. Goeasy, operating in Canada with a diversified, multi-channel model, is able to better control losses, even in high-risk segments. World Acceptance, in turn, highlights the limitations of lending directly to subprime customers without collateral, while also showing how active management can partially contain losses.

The homegrown management team

Credit Acceptance’s management team is characterized by remarkable cohesion and deep experience accumulated through years of service within the company. This continuity in leadership has allowed them to successfully navigate the complexities of the subprime auto finance industry, fostering a culture of internal growth and a deep understanding of the business model.

At the helm of the team is Kenneth Booth, President and CEO.

Kenneth Booth’s career at Credit Acceptance began in January 2004 when he joined the company as Director of Internal Audit. Within a few months, in May 2004, he was appointed Chief Accounting Officer.

His most defining and enduring role before assuming overall leadership was as Chief Financial Officer, a position he held since December 2004. For nearly 17 years as CFO, he was instrumental in the financial management of the company.

In May 2021, Kenneth Booth was appointed President and Chief Executive Officer, as well as a member of the Board of Directors.

As CEO, Kenneth has emphasized the importance of long-term relationships, a philosophy he attributes directly to the company’s founder, Don Foss.

He considers his predecessor Brett Roberts, to be a key mentor in his career, who taught him to “focus on what matters and execute flawlessly”. This mindset is reflected in his leadership, which strives for operational excellence.

Under his leadership, the company has achieved the largest outstanding loan portfolio in its 52-year history. He is currently 57 years old.

To assess his alignment with shareholders, we note that his annual compensation in 2024 was $1,000,000, with a 10% increase planned for 2025. He is the executive with the greatest skin in the game, currently owning 171,000 shares (1.5% of outstanding shares), valued at $86,355,000, —equivalent to 78 times his annual salary— indicating exceptionally strong alignment with shareholders.

In second place is Jay D. Martin, the current CFO.

He joined the company in September 20023 as SEC Reporting Manager and rose through the ranks: in 2005 to Director of Accounting, in 2009 he was appointed Vice President of Accounting and Financial Reporting, in 2012 he was promoted to Senior Vice President of Accounting and Financial Reporting, and in 2021 his role expanded to Senior Vice President of Finance and Accounting.

Finally, in January 2024, he was appointed Chief Financial Officer, culminating a career of more than 20 years preparing for the position. He is currently 51 years old.

To assess his alignment with shareholders, we note that his annual compensation in 2025 will be $615,000. He currently owns 27,166 shares, valued at $13,781,000 —equivalent to 22 times his annual salary— meaning his primary economic interest is aligned with that of shareholders: an increase in the share price, as this would grow his wealth more than his fixed remuneration.

Thirdly, we have Jonathan L. Lum, the current Chief Operating Officer.

He joined Credit Acceptance in 2002 as Senior Financial Analyst, subsequently holding positions in projects, external auditing and compliance. In 2011, he was appointed SVP of the Dealer Service Center. After 17 years of internal promotions, he reached the position of COO. He is currently 48 years old. His annual compensation is $650,000 and he owns shares worth $22,780,045, or 35 times his compensation.

Fourth, we have Daniel A. Ulatowski, Director of Sales.

He joined Credit Acceptance in 1996 as a Credit Analyst at the Dealer Service Center. Until 2003, he supervised teams at the Dealer Service Center. Between 2003 and 2006, he served as Regional Area Manager of Sales; between 2006 and 2007, he worked on Sales Training and Sales Operations; he later became Vice President of Sales, was promoted to Senior Vice President of Sales and Marketing in 2008, and ultimately, in January 2014, was appointed Director of Sales, a position he still holds today.

He is currently 53 years old. His annual salary is $770,000. He owns 54,054 shares, valued at $27,296,000, that is, 35 times his fixed salary.

And finally, we have Arthur L. Smith, Chief Analytics Officer.

Arthur joined Credit Acceptance in April 1997 and worked his way up through Manager of Dealer Risk, then Director in 2005, Vice President in 2007, Senior Vice President in 2008, and finally in 2023 Chief Analytics Officer.

He is currently 52 years old. His annual salary is $770,000. He owns 38,000 shares, valued at $19,190,000, or 25 times his base salary.

As we can see, the management team is highly aligned with the shareholders, as between them they hold 2.8% of the outstanding shares. This may seem like a small percentage, but we must bear in mind that this is a large company and that all of them started in relatively junior roles and progressed through the through their own efforts. As a result, many of them have a significant portion of their personal wealth invested in company shares, which means that —even if they do not control a large percentage of the equity— the key factor is the relationship between their net worth and their compensation.

Consequently, the management team has complete skin in the game.

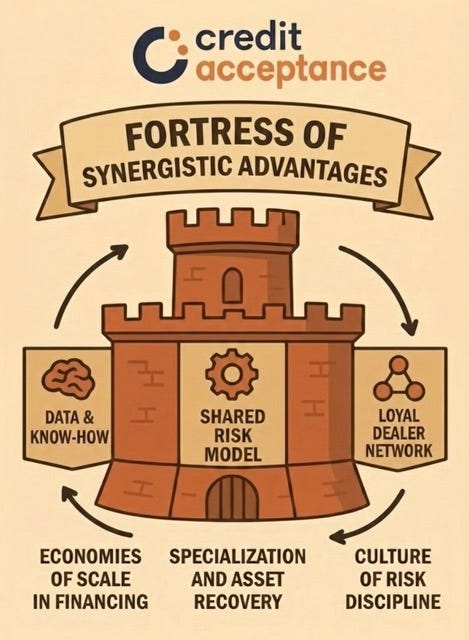

The competitive moat: A fortress of synergistic advantages

Credit Acceptance’s true competitive moat is not a single wall, but rather a fortress composed of multiple mutually reinforcing barriers. While other companies may excel in one area, Credit Acceptance’s durability lies in the synergistic interaction of its advantages, creating a system that is exponentially more difficult to replicate than the sum of its parts.

The system is based on three fundamental pillars that operate in perfect harmony:

50 years of data and know-how

Credit Acceptance’s most valuable

asset does not appear on its balance sheet: it is the knowledge accumulated over five decades of underwriting loans in the subprime segment.

The company has built a massive, proprietary database that records the payment behavior of millions of high-risk profiles.

This is not a simple repository, but a dynamic risk laboratory. Each new loan feeds and refines its algorithmic models, creating a virtuous circle: more data generates smarter predictions, enabling almost surgical precision. In a business where a single point of delinquency can wipe out margins, this predictive intelligence is decisive and constitutes an almost insurmountable barrier.

The risk-sharing model

This is the economic engine that translates data into a unique value proposition. Unlike traditional financial institutions that assume 100% of the risk, Credit Acceptance distributes it.

The mechanism is simple but powerful:

When a customer pays on time, the dealer participates in future profits.

If they default, they bear part of the loss.

This approach aligns incentives in an extraordinary way, motivating the dealer to be the first and most effective filter.

The loyal dealer network

This is the exclusive distribution channel that the model has built. Risk sharing transforms a transactional relationship into a long-term strategic partnership.

The result is:

High switching costs for dealers.

An extraordinarily loyal network of partners.

A channel that is difficult to replicate, which competitors cannot buy, only build over time.

The virtuous circle: How the system feeds back on itself

The magic lies in the feedback between the three pillars:

The dealer network generates loans that feed the data.

The data refines the risk model, making it more accurate and profitable.

A more reliable model strengthens the loyalty of the network, which in turn expands and generates even more data.

This virtuous circle is the essence of Credit Acceptance’s competitive moat.

Additional advantages that reinforce its strength:

Economics of scale in financing: despite having speculative-grade debt (BB/Ba3), the predictability of its model ensures access to cheaper capital than its competitors.

Specialization and asset recovery: with the vehicle as collateral and standardized processes, the company discourages default and converts high-risk loans to profitable assets.

A culture of risk discipline: a corporate DNA forged over 50 years, which prioritizes prudence over growth at any cost, and which has enabled it to survive and thrive in crises such as those of 2008 and 2020.

In conclusion: Credit Acceptance’s competitive moat does not depend on a single advantage, but rather on an interconnected system of data, incentives, and relationships, backed by its culture and experience, which makes the company a unique player that is very difficult to replicate in the subprime sector.

Risk and weakness analysis

Any solid investment thesis must analyze the counterarguments head-on. Despite its formidable competitive strength, Credit Acceptance operates in a complex market and faces significant risks that partly justify its persistently discounted market valuation. A bearish investor would focus their criticism on five key areas.

Regulatory and legal risk

This is undoubtedly the greatest risk. Credit Acceptance’s business model, which relies on high interest rates (often 20-30%) to offset high risk, operates in a gray area that attracts constant scrutiny from agencies such as the Federal Trade Commission and the Consumer Financial Protection Bureau. A regulator could determine that is rates or collection practices are predatory, imposing millions in fines that erode capital. Furthermore, they could force structural changes to its model, such as limiting maximum interest rates or restricting its vehicle recovery methods. Regulatory action of this magnitude would not only affect future profits but could damage the core of its competitive advantage.

Economic and cyclical risk

The company is almost entirely dependent on the financial health of subprime consumers. Although its models have proven resilient, even in 2008, a skeptic would argue that they have not faced a prolonged recession in modern times combined with high inflation. In a scenario of structurally high unemployment (above 8-10%), delinquency could skyrocket beyond the company’s historical forecasts. At the same time, an economic crisis would depress the used car market, drastically reducing the recovery value of repossessed vehicles. This double impact —lower collections and lower collateral value— could squeeze margins to unsustainable levels.

Financing risk and leverage

Credit Acceptance’s engine is fueled by its ability to package its loans and sell them on the securitization market (ABS). Its speculative-grade or high-yield rating (BB/Ba3) is a constant reminder that capital markets perceive significant risk. In a liquidity crisis such as that of 2008, the ABS market could shut down or become prohibitively expensive. If Credit Acceptance cannot securitize its loans at a reasonable cost, its ability to originate new loans would come to a screeching halt. Its high level of leverage makes it vulnerable to a credit crunch, where a sudden increase in the cost of capital could destroy the profitability of their business.

Cultural and succession risk

The culture of risk discipline, inherited from founder Donald Foss and maintained by the current management team, is an intangible asset. The risk lies in the possibility that this culture will dilute over time. While the current team are “home-grown guardians”, a future generation of leaders, pressured by Wall Street to accelerate growth, could be tempted to relax strict underwriting criteria or squeeze dealers, damaging the partnership model. Even a small deviation from the model that has worked for 50 years could initiate a slow but irreversible erosion of the competitive moat.

Structural risk: The transformation of the automotive sector

Finally, a longer-term risk lies in the structural changes that the automotive industry itself is undergoing. Credit Acceptance’s business model depends fundamentally on the predictable dynamics of the used combustion engine vehicle market. Electrification could drastically alter the residual value of financed cars. Even more disruptive, the eventual arrival of autonomous vehicles and mobility-as-a-service models could completely alter the concept of individual car ownership, structurally reducing demand for long-term subprime financing.

Valuation

Why is the share price the same as in 2019?

Credit Acceptance has increased its revenue by an average of 7% since 2019. Despite this, its share price remains at the same level as in that year. This is because its profit margins have been affected since 2022 by a significantly lower return on loans granted. The causes were intense competition, which coincided with the end of federal stimulus payments, the end of unemployment benefits, peak vehicle prices and rising inflation.

The company expects to recover profitability with new credits and, as the 2022 loans mature, for margins to return to average levels.

Optimistic scenario

If we estimate the expected value for 2030, revenues of $3.136 billion could be generated, which would be a conservative annual growth rate. With a mean reversion of profit margins of 35%, Credit Acceptance would be generating $1.097 billion in profits. Estimating that they repurchase 5% of the shares per year (a conservative estimate, considering that in Q2 2025 alone they repurchased 4.2%), there would be 8,876,800 shares in circulation.

This would generate earnings per share of $123. Valuing the company at 12 times earnings (its historical average), the price per share would be $1,482. This implies an annual return of 25% from the current price of $460 until the end of 2030.

Conservative scenario

If we make a conservative valuation, assuming no growth and that profit margins fail to return to the average —remaining 1,000 basis points below (a 25% shortfall) — we would expect revenues of $2,308 million with a profit of $577 million. Assuming the company continues share repurchases, but at a below-average pace (3% per year), there would be 9,954,000 shares outstanding.

This would generate earnings per share of $58, which, if we value the company at 10 times earnings, would give us a price of $580. This would generate an annual return of 5%, showing a considerable margin of safety.

Final thought: A misunderstood force

Credit Acceptance represents an apparent paradox in the investment world: a high-quality business operating in a market segment with low perceived quality. For more than fifty years, the company has demonstrated extraordinary resilience, not only surviving multiple economic crises that wiped out its competitors but emerging from then stronger than ever. Its success is no accident; it is the result of having built an almost impregnable competitive strength for the more than 140 million U.S. consumers excluded by the traditional financial system.

The company’s true competitive advantage does not lie in a single strength, but rather in the perfect synergy of its system. Its 50 years of data give it unmatched predictive risk intelligence. Its risk-sharing model transforms dealers into aligned partners. And its loyal dealer network is the result of that engine: an exclusive asset protected by high switching costs. At the helm of this fortress stands a homegrown management team whose incentives are fully aligned, as demonstrated by its long-standing and aggressive buyback policy.

Of course, a fortress of this caliber does not go unnoticed without generating skepticism. The main risk —and the reason for its chronic undervaluation in the market— is regulatory. However, this risk is also the source of the opportunity. It is the toll the market demands for investing in such a dominant business model.

Ultimately, investing in Credit Acceptance is a bet on the continuity of a proven system, managed by an experienced and disciplined team. It is an investment for the patient investor, one who can look beyond negative headlines and recognize the structural quality of a business that thrives where traditional banking does not dare to compete. Credit Acceptance is not merely a finance company; it is a piece of infrastructure addressing a structural market failure and a formidable compounding machine for investors who understand it.

Final verdict and positioning

As we can see, the optimistic scenario gives us an expected annual return of 25%, while the more conservative scenario still offers us a 5% annual return. At $460 per share, the price at the time of this valuation, I consider it an excellent price to buy. In my case, it is the seventh-largest position in my portfolio, representing 5.6%, and I have recently been increasing the position at $458.

This concludes my thesis on Credit Acceptance.

If you liked it or think it might be useful for someone else, feel free to share it.

Best regards!

Disclaimer:

The content of this publication is for informational and educational purposes only and does not constitute investment advice or an invitation to buy or sell securities. The author assumes no responsibility for decision made based on this information. Anyone interested in investing should have adequate training or seek the advice of a duly authorized professional.